Investigating Credit Card Fraud, Part V, Final Models

I complete the hyper-parameter optimisations for the random forest and xgboost models. I then create a final model using these values to produce AUCs of 0.852 and 0.872.

Other posts in series

Forest model, hyper-parameter selection

I tidied up the code from yesterday to allow me to optimise for more than one parameter at once. For each combination of hyper-parameters, I obtained 20 different AUCs (by using five 4-fold cross validations). The results were stored in a pandas dataframe. The code for this is at the bottom of the page.

I then averaged over all the folds and sorted the results. The code for this and the output is below.

auc_forest.max_depth.fillna(value = 0, inplace = True)

auc_forest_mean = auc_forest.groupby(['n_estimators', 'max_depth', 'max_features']).auc.mean()

auc_forest_mean.sort_values(ascending = False).head(20)

n_estimators max_depth max_features auc

50.0 0.0 10.0 0.774015

50.0 10.0 0.774015

60.0 0.0 10.0 0.772589

50.0 10.0 0.772589

10.0 10.0 0.772573

50.0 10.0 10.0 0.772328

40.0 10.0 10.0 0.771290

80.0 0.0 10.0 0.771108

50.0 10.0 0.771108

40.0 0.0 10.0 0.770744

50.0 10.0 0.770744

50.0 0.0 7.0 0.770522

50.0 7.0 0.770522

80.0 10.0 10.0 0.770487

50.0 10.0 7.0 0.770472

60.0 50.0 7.0 0.770472

0.0 7.0 0.770472

10.0 7.0 0.770025

40.0 50.0 5.0 0.769278

auto 0.769278

A few things were found by doing this:

- The best options for the hyper-parameters are n_estimators = 50, max_depth = None and max_features = 10.

- max_depth = None and max_depth = 50 produced the same models. This means that maximum depth achieved without any limits is less than 50.

- max_features = auto and max_features = 5 produced the same models. This is obvious in retrospect: auto means taking the square root of the number of features, and we had about 30 features.

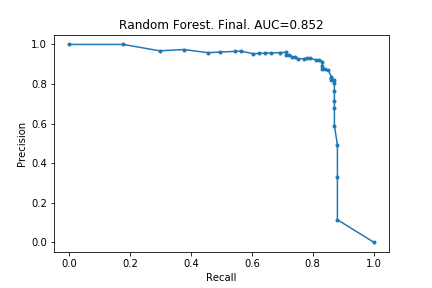

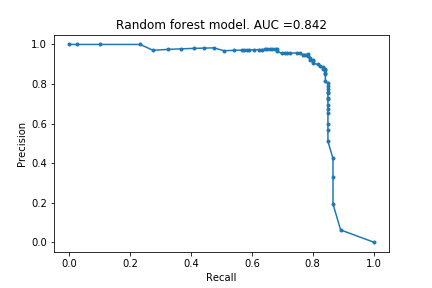

Forest model, final model

Using these hyper-parameters, I created a the final Random Forest model. The precision-recall curve is below:

For comparison, the very first random forest model is also included. As can be seen, there is an improvement but a seemingly minimal one. Based on examples I have seen elsewhere, these minor improvements are what can be expected from hyper-parameter optimisations.

XGBoost model

I repeated the process above for XGBoost models. The best parameter settings were as follows:

n_estimators max_depth learning_rate auc

50.0 5.0 0.05 0.761125

100.0 5.0 0.02 0.760002

50.0 10.0 0.05 0.759094

15.0 0.05 0.758146

100.0 10.0 0.02 0.757185

15.0 0.02 0.756748

200.0 10.0 0.02 0.747032

15.0 0.02 0.743830

50.0 15.0 0.10 0.742954

10.0 0.10 0.739922

100.0 10.0 0.05 0.737840

15.0 0.05 0.737013

50.0 10.0 0.02 0.729299

15.0 0.02 0.729239

5.0 0.02 0.729049

200.0 5.0 0.02 0.727433

50.0 15.0 0.30 0.726696

5.0 0.20 0.726479

100.0 5.0 0.20 0.724851

15.0 0.30 0.722728

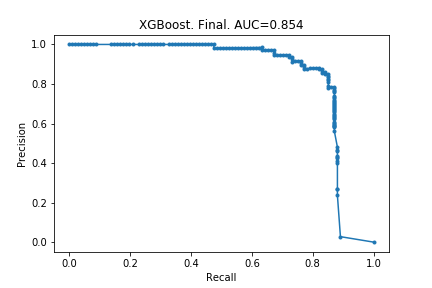

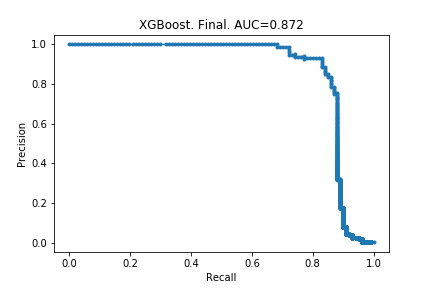

Using the settings from the top row, I created my final model, whose precision-recall curve is below. I have included the original curve, too.

!! After doing the optimisations, the model became worse! The AUC decreased by 0.002. The explanation for this must be that removing 99% of the data actually changes the behaviour of the model.

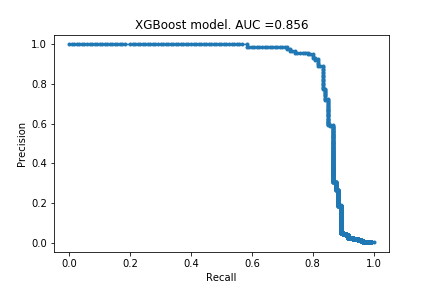

I re-did the process but only removing 90% of the data (recall from Part II that in XGBoost, removing 90% of the data did not decrease performance that much). This time, the optimal settings were as follows:

n_estimators max_depth learning_rate auc

200.0 10.0 0.10 0.816130

5.0 0.10 0.815648

100.0 5.0 0.10 0.807745

10.0 0.10 0.806940

200.0 10.0 0.05 0.805212

5.0 0.05 0.801478

50.0 10.0 0.10 0.797015

5.0 0.10 0.794567

100.0 5.0 0.05 0.793189

10.0 0.05 0.792732

200.0 5.0 0.02 0.785652

10.0 0.02 0.783957

50.0 5.0 0.05 0.779087

10.0 0.05 0.778968

100.0 5.0 0.02 0.776565

10.0 0.02 0.775092

50.0 5.0 0.02 0.761190

10.0 0.02 0.760388

The optimal parameters changed (thankfully!). I then re-created the final model and this time there was an improvement:

Next time

My next blog post will be the final one in this series. I will summarise what I have done and what I have learnt. I will also have a look at what others did and see what I can learn from them.

The code

The code is provided for the Random Forest optimisation. The code for XGBoost is similar.

# import modules

import numpy as np

import pandas as pd

from sklearn.model_selection import train_test_split, KFold

from sklearn.metrics import precision_recall_curve

from sklearn.metrics import auc

from matplotlib import pyplot as plt

import seaborn as sns

from sklearn.ensemble import RandomForestClassifier

from xgboost import XGBClassifier

import itertools

#import data

data = pd.read_csv("creditcard.csv")

y = data.Class

X = data.drop(['Class', 'Time'], axis = 1)

#create train-valid versus test split

Xtv, X_test, ytv, y_test = train_test_split(X,y, random_state=0, test_size=0.2)

# create function which takes model and data

# returns auc

def auc_model(model, Xt, Xv, yt, yv):

model.fit(Xt,yt)

preds = model.predict_proba(Xv)

preds = preds[:,1]

precision, recall, _ = precision_recall_curve(yv, preds)

auc_current = auc(recall, precision)

return auc_current

# create options for hyperparameter

n_estimators = [40, 50, 60, 80]

max_depth = [None, 5, 10, 50]

max_features = ['auto', 3,5,7,10]

random_state = range(5)

# create frame to store auc data

auc_forest = pd.DataFrame({'n_estimators': [],

'max_depth': [],

'max_features': [],

'fold': [],

'auc': []

})

# loop through hyper parameter space

for n, md, mf, rs in itertools.product(n_estimators, max_depth, max_features, random_state):

kf = KFold(n_splits = 4,

shuffle = True,

random_state = rs)

model = RandomForestClassifier(n_estimators = n,

max_depth = md,

max_features = mf,

random_state = 0)

i=0

for train, valid in kf.split(Xtv):

Xt, Xv, yt, yv = Xtv.iloc[train], Xtv.iloc[valid], ytv.iloc[train], ytv.iloc[valid]

# remove 99% of the non-fraudulent claims from training data to speed up fitting

selection = (Xt.index % 100 == 1) | (yt == 1)

Xt_reduced = Xt[selection]

yt_reduced = yt[selection]

auc_current = auc_model(model, Xt_reduced, Xv, yt_reduced, yv)

auc_forest.loc[auc_forest.shape[0]] = [n, md, mf, 4*rs+i, auc_current]

i+=1